Section 1.3 Money Psychology

At the end of the day, financial well-being is large a product of the decisions we make with our money. Knowing all about the world of finance the consequences of decisions is not enough to maintain financial health. You must also know why you make the decisions you do. Having an understanding of yourself will help you keep on making sound financial decisions and avoid poor ones.

Subsection 1.3.1 Money Personality

You have seen a glimpse of money personality and have thought about your own. Your money personality shapes your beliefs and values regarding your finances (and even the whole financial world). These beliefs and values directly affect how you think about money. For example, suppose you have $10,000 saved into an account. A person who is a saver will likely value security over spending and would be more inclined to continue saving or investing that money. A money worshipper may value financial status and be more inclined to spend the money on something like a down payment for a fancy car. A money spender may value exciting experiences and see that money as an international vacation.

The point is that it helps to know yourself around money. Suppose you have that $10,000 and \textit{know} you shouldn’t spend it, but you find yourself unable to stop thinking about all you could buy with it. Realizing that your money personality may drive you more toward spending can allow you to be more mindful of your feelings. Realize that your feelings are not wrong. Feel your feelings. But go with what you know is the best option for you. With practice, this becomes easier and easier.

Subsection 1.3.2 Money Biases

Everyone is unique, right? Well, some aspects of money psychology are so common that there are names for them. In fact, many advertisements and salespeople utilize some of these aspects to manipulate you into spending your money. We’ll discuss these tactics when we explore scams and manipulation.

Generally speaking, a bias is a thought, opinion, practice, etc. that is so imbedded in your brain that it affects your behavior without you realizing it. A bias is not as simple as “I like X better than Y.” They are subtle, but powerful. Most people are unaware of their biases until those biases are confronted. Even then, many people choose not to accept their own biases. We will go through some of the most common financial biases.

Society Bias. Have you ever thought about needing the latest model of a phone, even though yours still works fine? Is it the extra 26 minutes of battery life? Is it the extra 0.4MP resolution on the camera? No. It’s about status. Cellular phones and smartphones have been symbols of status since their creation. (Seriously, look at who bought the first cellular phones.) Status symbols can drive many of us to make purchases that stretch our budgets. Many people buy the largest homes their budgets can possibly afford when a smaller one would be just as functional. Many people dine at expensive restaurants mostly for the opportunity to post a photo of their meal to social media. Similarly, some people buy the latest smartphones so that they can have the largest number available.

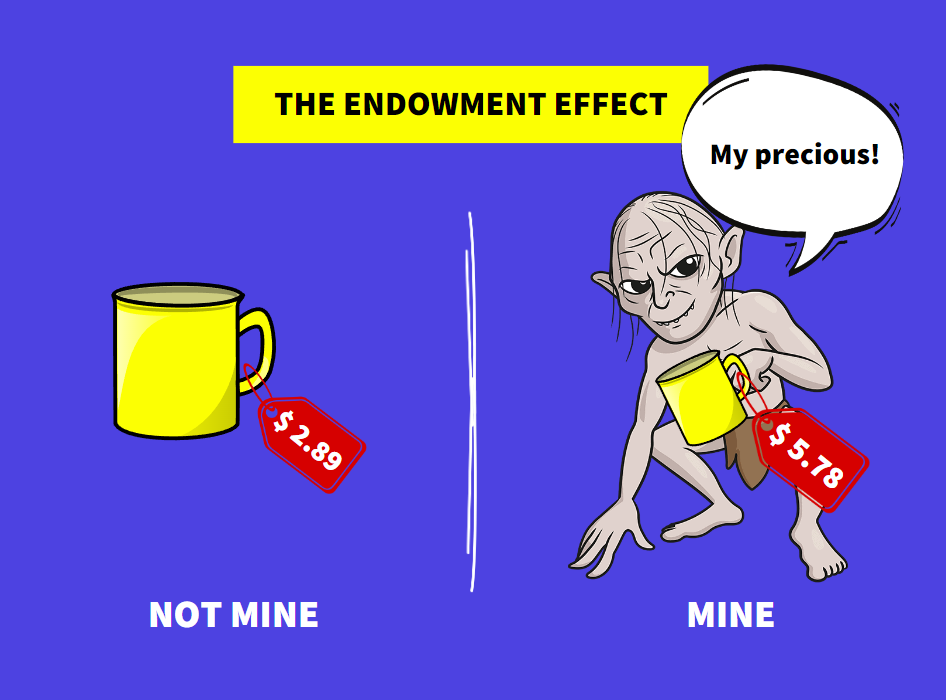

Endowment Effect. The endowment effect is less about buying and more about selling. Have you ever run a garage sale (or “tag sale” for you New Englanders) or tried to sell a car of phone? That feeling you get when you are offered a price less than what you feel is owed is the endowment affect. An interesting commonality in human psychology is that once we own an item we feel as though it is worth more.

Imagine this scenario. You buy a car that has a value of $25,000. However, the second you sign the paperwork and own the car, the car’s value drops to $20,000 because the car now has a “previous owner” and has depreciated. How does that make you feel? Are you feeling, “Oh, that totally makes sense that my car is worth less”? Or are you feeling, “That’s bull. If I haven’t driven the car, it’s still worth what I paid for it”? Probably the latter. The thing with the endowment effect is that it can cause people to hold onto items that they really want to sell. Rather than earning some cash on an item you want to sell, you get no money and need to keep owning your item.

Loss Aversion. One of the workers behind the endowment affect is loss aversion, but loss aversion is a mental bias all its own. In general, people prefer to avoid losing money rather than making gains. Don’t believe me? Think about this scenario. You can play a game. You have a 75% chance of winning it. If you win, you double your life savings. If you lose, you lose all your life savings. Do you play the game?

From a mathematical standpoint, the answer is clearly “yes!” However, most people will not take that bet because of loss aversion. Loss aversion has the potential to make you miss out on financial opportunities and investment gains. Now, a 25% chance of losing your life savings is a bit extreme, but loss aversion can affect much “smaller” financial decisions. Here’s a common example with stocks. When investors see a good gain in a day, they are happy but not shocked. However, when a loss of a similar magnitude happens, the feeling of that loss hits much harder. Many investors will then pull their money out of investments when they see a sudden loss. However, selling a stock when it hits a low is generally not a good idea. (On the other hand, some stocks will continue to decline, and investors may choose not to sell due to loss aversion.)

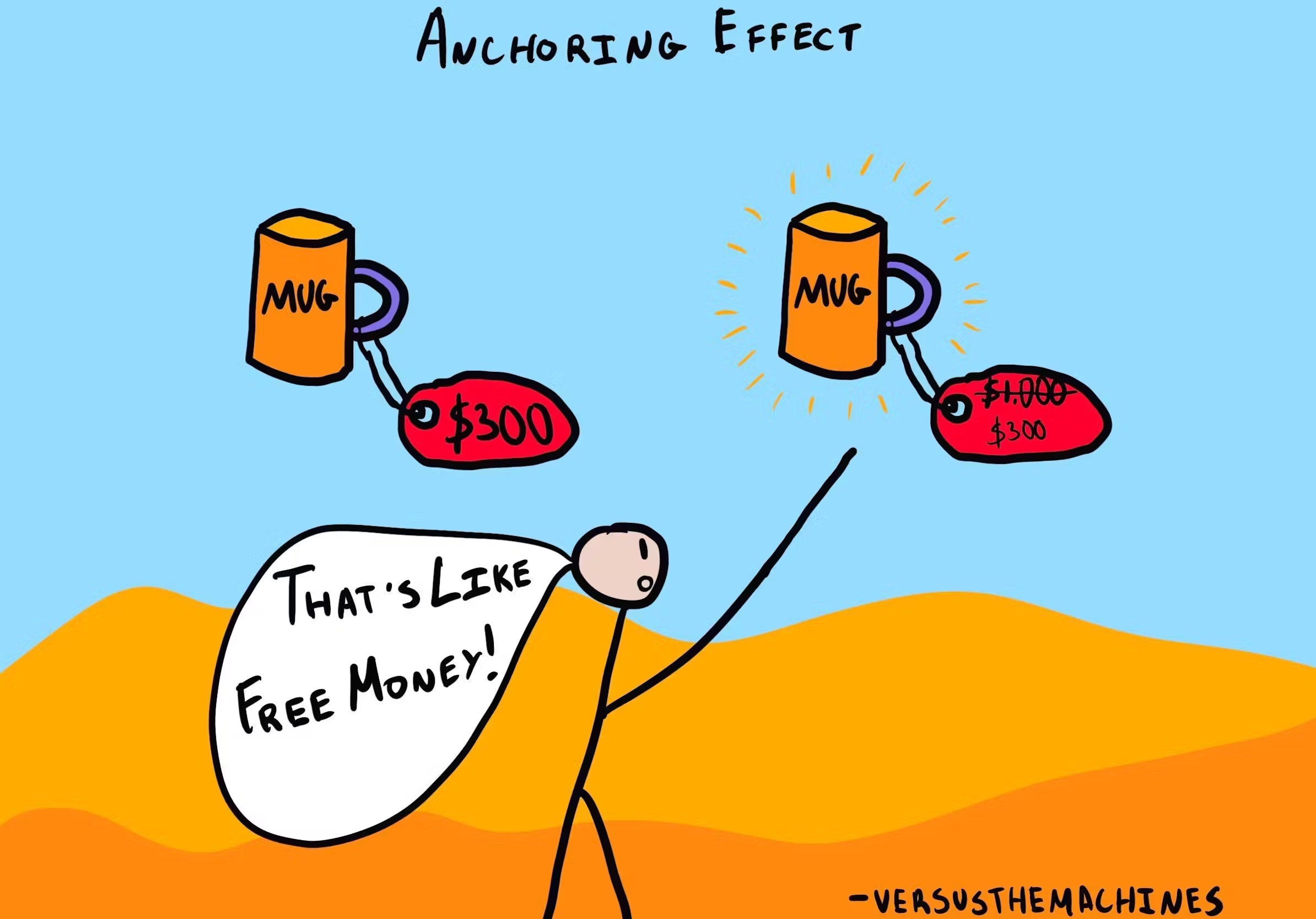

Anchoring Bias. Here is a huge one that is the foundation of a lot of advertising schemes. (We’ll dig in more later as to how.) Anchoring bias is now closely tied to the idea of a “sale” or “deal.” Seeing a product being offered for a price less than it was originally can make us want to buy that product, regardless of whether it worth that much.

Do you notice that “sale” tags always tell you the price before the sale. It’s to trigger your anchoring bias. There is a lot to discuss regarding manipulation and anchoring, but that will come in a later week. For now, be aware that this bias exists. When making decisions on what to buy, do not concentrate on what was. Concentrate on what is. It doesn’t matter that the pack of Oreos is usually $4 and is $3 today. Were you going to buy Oreos anyway? Is $3 the price you’re willing to pay?

Present Bias. It is usually easier to concentrate on what you’re feeling now compared to what you may feel in the future. Present bias is the concept of living in the present. Living in the present is great for mindfulness, but it can be detrimental to making future plans. Living too much in the present can cause overspending on things you want now rather than saving for the future. Of course, it isn’t good to live totally in the future and become a miser. Working with your present bias takes practice and hard work. Your brain is hard-wired to want what you want now. Delaying gratification for a much stronger sense of happiness takes conscious effort. Try to get into the habit of asking what you’re giving up by spending money now. By buying the latest model phone now instead of skipping a generation, what financial goals or milestones are you delaying? By ordering that doughnut at Dunkin’, what nutritional goals are you giving up? You do not need to sacrifice everything that makes you happy, but you need to have an eye toward the future. Your future self will thank you.

Confirmation Bias. Have you ever scoured the Internet looking for opinions to help you make an important decision? Often, people find a scenario in which most of the information tells them not to make a certain choice, but they only really accept the small bit of information that supports making that choice. This is confirmation bias at work.

Here’s an example (not really financial). I am currently debating whether to get surgery on my spine to help with neurological pain. I’ve been debating this surgery for three years. When I have particularly bad flare-ups, I look for people’s opinions and experiences with the surgeries. I find myself much more likely to read stories of successes rather than warnings or bad experiences.

This is likely because that main pain has made me unconsciously decide to get the surgery, and I am looking for confirmation of that opinion. Confirmation bias pops up constantly when making financial decisions. If you find yourself looking at information and only clicking on certain articles, posts, or sites, there is likely confirmation bias at work. It is important to remain objective as you make important decisions and accept all credible information as credible.

Just as a point of reference. Confirmation bias exists everywhere. It is one of the cornerstones of racism, conspiracy theories, homophobia, tribalism, etc. It is a really, really strong bias that every person on this earth has. Being more aware of it can help you make decisions that are actually in your own interest rather than making poor decisions and mentally-manipulating what you see to confirm that poor decision.

Affinity Bias. Related to confirmation bias is affinity bias. Affinity bias can be thought of as brand loyalty that can cause some inefficient financial decisions. For example, many adults ignore cheaper store-brand items in grocery stores (or even refuse to try shopping at a place like Aldi’s); they instead only purchase items from brands they recognize. Sometimes there may be sound reasons for this restriction, but often the differences are minimal. For example, many store brand items are actually manufactured in the same factory as name-brand ones. The only difference is packaging.

Affinity bias doesn’t have to be objectively bad. Many people make conscious efforts to support or not support certain businesses or products. For example, many people refuse to shop at Walmart, despite it being cheaper, because they do not support the low wages paid to employees or the forced closures of small businesses. What is important is for you to be aware of affinity bias and make conscious choices that fit with your preferences and financial goals.

Herd Mentality. Very much related to social bias is herd mentality. You have likely heard of it before. It’s the thing everyone says people different from them follow and is what hipsters claim to be immune to. We are all under the effect of herd mentality. It’s easy to see when other people are following a herd, particularly when we don’t like that particular herd. It is much harder seeing when you are following a herd.

The consequences of herd mentality in the financial world (and beyond) are many. Herd mentality can cause you to buy something you really don’t need or even convince you that you do need an item. It can cause investors to buy stocks that have been on the rise right before a “bubble burst.” In the modern world, the two most prevalent sources of herd mentality are in rating systems and influencers. Did you most recipe ratings online are fake? Did you know most Amazon reviews on a product are not for the actual product you’re interested in? Yet they’re important factors in determining our behavior. Speaking as someone who grew up before social media, I cannot tell you how bonkers I find the idea of watching an influencer. Yet followers beget more followers, which is the very concept of herd mentality.

Subsection 1.3.3 Activity: Think About Your Biases

Pick three of the biases above that you have experienced in some way. (If you think you haven’t been influenced by these biases before, think harder.) For each bias, briefly describe a time when that bias affected your thinking or behavior. Briefly reflect on how being mindful of those biases could lead (or have led) to better decisions.

Subsection 1.3.4 Debrief

One thing to notice is that thinking about weaknesses in the way we think is difficult. That’s because of the biggest bias of all - self-bias. We trust our own thoughts more than ones that conflict with them. That’s ok; it’s part of being human. However, like it or not, biases affect your behavior. Some may be more prone to certain biases than others, but bias is part of the human condition. From a financial standpoint, learning to recognize your own biases can help you make more informed and beneficial decisions about your money.