Section 2.2 Budgeting Rules

In this section, we’ll explore a few popular budgeting rules. There are general strategies for planning to spend your paychecks. Not all rules will fit everyone’s situation, so it can take some trial-and-error to find one that works for you.

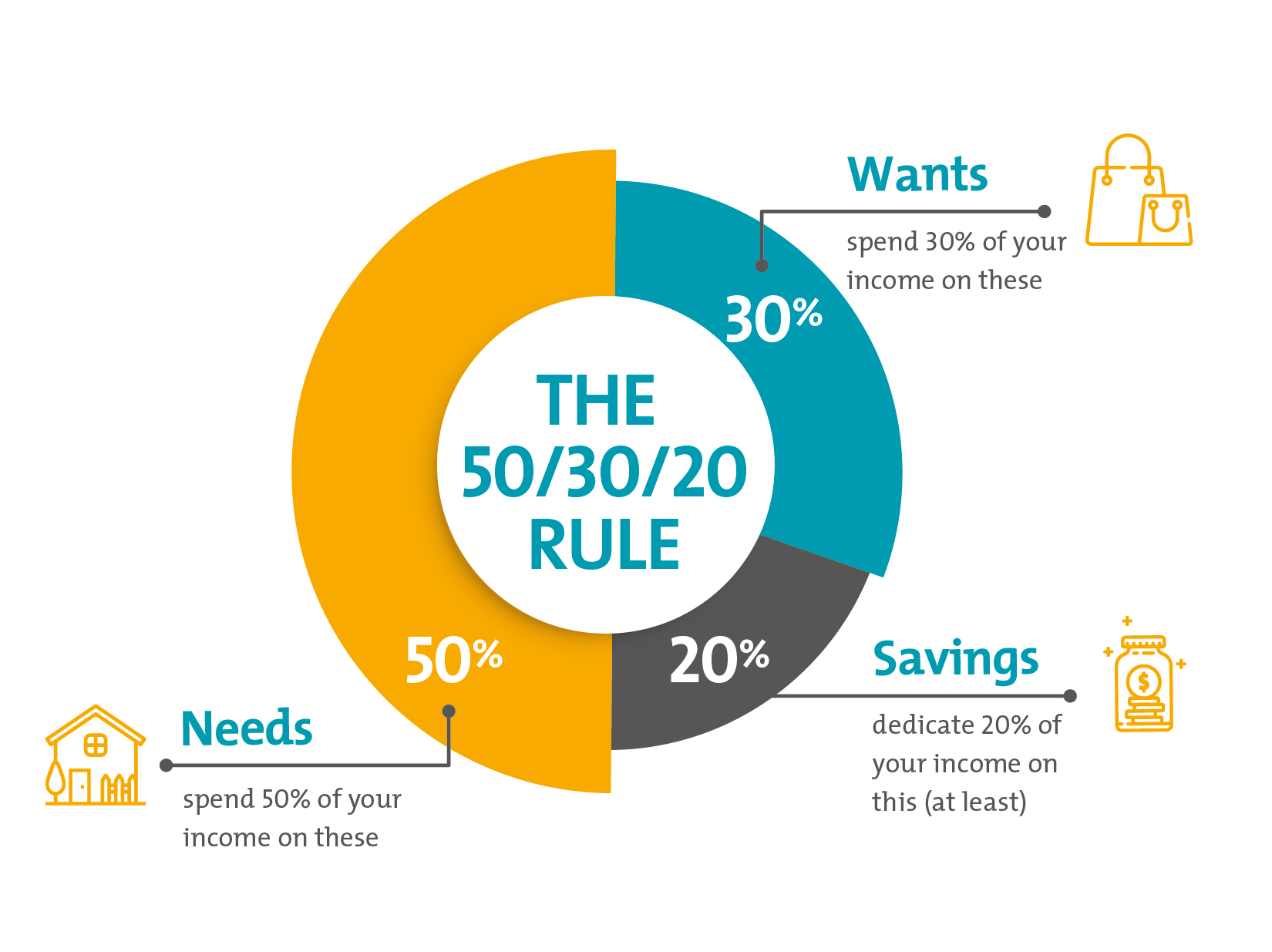

Subsection 2.2.1 The 50-30-20 Rule

Here is the rule. Your after-tax income (“take-home pay”) should be allocated so that 50% is spent on “needs,” 30% is spent on “wants,” and 20% is saved. That’s it. Let’s break down these three categories.

Needs - A need is a necessity that you cannot do without. Housing, utilities, food, supplies, insurance, clothing, and transportation are examples of things considered necessities. Other things can definitely be considered “needs,” based on your individual situation.

Wants - A want is something that you would like to have but isn’t strictly necessary for your survival. Eating out, entertainment, coffee, luxury items, and cosmetics are examples of things considered wants.

Savings - A savings item is simply an account in which you put money you do not spend that can be used for the future. Retirement accounts, savings accounts, and swear jars are all examples of things considered to be savings items.

Sounds simple, right? Here is one of the biggest barriers to the 50-30-20 rule. Most people are reluctant to label some desirable items as a “want.” Thinking to yourself, “I couldn’t live without coffee,” doesn’t make it a need. If you live where there is robust public transportation, owning a car may not be considered a need. Pet supplies are tricky. Is owning a pet a necessity? Most people with pets are hesitant to say no. What about Internet access? It may be a necessity, but is the highest speed possible a necessity?

Here is an important truth. If the thought of not having something makes you uncomfortable, that doesn’t make the thing automatically a necessity.

Here some examples of things I’ve heard from people in my life this particular week (at the time I wrote this section):

- “I just need Taco Bell for my mental health. It’s my comfort food.”

- “I couldn’t survive without Door Dash.”

- “We can’t live anywhere that won’t allow the ‘sweets.’” (“Sweets” are her cats. For context, they’ve been without housing for a year, and this was in response to an opportunity to get into an affordable place.)

Subsection 2.2.2 Activity: Classifying Spending

Let’s practice categorizing things as needs, wants, or savings. For each item/scenario, classify each as a need, a want, or savings. Pick only one. For each, explain your answer in one sentence.

- 401-k contributions automatically taken from your paycheck.

- Going out to dinner after a really stressful week at work.

- Car insurance.

- Giving an allowance to your child.

- Lottery tickets.

- Buying stocks.

- A Netflix subscription.

- Paying for the repair of your refrigerator.

- Cleaning supplies.

- A limited-edition collector’s item.

- The latest Taylor Swift album.

- Child-support payments.

Subsection 2.2.3 Debrief

We’re some of these tricky? I hope so. If fact, you may have come up with different answers as others. Some may even depend on the context you imagine. Here are my answers, in order: savings, want, need, want, want, savings, want, need, need, want, want, need.

Subsection 2.2.4 Allocating Money under the 50-30-20 Rule

Once you can categorize spending, you can get into the actual meat of the 50-30-20 plan. It can be tedious, and it requires you to have a very detailed and realistic record of your spending. Here is the rough steps in creating your budget.

- First, determine how much money you make in a month. (You can also do it by week or by paycheck. However, since bills are usually paid monthly, it is best to budget monthly.) Your paycheck will likely be the biggest source of income, but there may be other sources. Any money that you take in counts. Make sure to only count what you actually get (the “net” amount). For example, if you work a job for 40 hours a week at $21 per hour, your weekly pay is \(40 \times 21 = $840\text{.}\) However, that is not what you actually get because of taxes. To simplify things, if you have an annual salary, take that amount and divide by 12 your monthly pay. If you are paid bi-weekly, multiply your paychecks by 2 to get your monthly amount. For weekly paychecks, multiply by 4. If your paychecks vary from check to check, do your best to come up with a monthly average.

- Determine how much you can allocate to each category. For needs, we want 50% of your income. So, take your monthly income and multiply by 0.5. For wants, take your income and multiply by 0.3. For savings, take your income and multiply by 0.2. For example, suppose your monthly income is $3,400. Then you can have \(3,400 \times 0.5 = \$1,700\) devoted to needs, \(3,400 \times 0.3 = \$1,020\) devoted to wants, and \(3,400 \times 0.2 = \$680\) put into savings.

- Make a list of everything you spend money on in a month. You can group things into categories. For example, don’t list out items from the grocery store. Just have one “groceries” item. This is probably the hardest step. Everything counts. Do you buy a mocha only once or twice a week? That’s $20-$40 from your monthly income that you can’t ignore. Be honest with yourself. It may be necessary to look at your credit card bill or debit card statement to really see where and when you spend money.

- Categorize your items as needs, wants, or savings.

- Add up how much you spend in each category and compare to what amounts you’re allowed. If you over-spend in a category, you may need to change how your finances work, which we’ll go over shortly. Also note that putting too much into savings is not really grounds for alarm. Only if you feel like you’re not enjoying how you’re spending money should you worry about saving too much.

At the end of this section, I’ve created a budget spreadsheet you are free to use.

Subsection 2.2.5 The 80-20 Budget Plan

Sometimes, the 50-30-20 plan doesn’t work. This is becoming more true for the millennial, Z, and alpha generations as housing costs are increasing more than wages. It is very common to find yourself in a position where you simply can’t allocate only 50% of your paycheck to needs. One solution to that is to “combine” needs and wants into one category in which you allocate 80% of your take-home pay to needs and wants and 20% to savings.

Notice something. This version of the 50-30-20 plan essentially lowers the amount for wants in exchange for needs. It still requires you to save 20%. Generally, you should always prioritize saving over wants. It is vastly more important that you save for unexpected future expenses and retirement rather than spend on things you don’t need.

The main benefit of the 80-20 budget is increased flexibility over the 50-30-20.

The increased flexibility of the 80-20 plan does come at a cost. Flexibility allows greater freedom. Greater freedom allows more opportunity to stray from the budget. Simply put, people want wants and do not want to save. It is really easy for the 80-20 plan to become the 100-0 plan. (The 100-0 plan is not a real plan. Please don’t do it.) If you find yourself in a situation where 70% of your paychecks go to necessities like housing, student loans, food, etc., it can be difficult to spend only 10% on stuff you want. Feeling overworked or overstressed can make wants feel like needs.

Under the 80-20 budget plan, you should still classify spending as needs, wants, and savings. it is important for your brain to see that certain spending behaviors are non-essential.

Subsection 2.2.6 The Envelope System (A.K.A. “Cash Stuffing”

One of the most classic budgeting methods is the envelope system. On social media, this is now often called “cash stuffing.” Traditionally, the envelope system requires you to take your entire paycheck in physical cash and allocate that cash into different envelopes for different spending activities. You could have a “rent” envelope, a “student loan” envelope, a “groceries” envelope, a “Dunkin”’ envelope, a “savings” envelope, etc.

Once you distribute your cash, you do your best not to take money from an envelope for any reason other than its intended purpose. For example, don’t take money out of your “groceries” envelope because you want to go out to eat.

This budgeting method is great for people who tend to over-spend on non-necessities. If you find yourself spending money on things you know you shouldn’t, you can try the envelope method. Physically keeping money in labeled envelope can help you see and adhere to your money’s intended purpose. Further, the process of allocating money physically helps you see exactly where your money is going. If you find yourself transferring money from one envelope to another, you are physically seeing that you’re not sticking to your budget.

One big negative drawback of this system is that it requires you to have your money in cash. However, most bills are paid electronically these days. It also requires you to physically go to a bank or ATM to get cash. Further, your paychecks are usually more frequent than billing cycles. So, you have to learn to put parts of needed bill amounts in an envelope with each paycheck. Also, keeping physical cash around your place can be unsafe.

There are some apps available that can help set up a digital “envelope system.” We’ll discuss budgeting apps later in this week’s material.

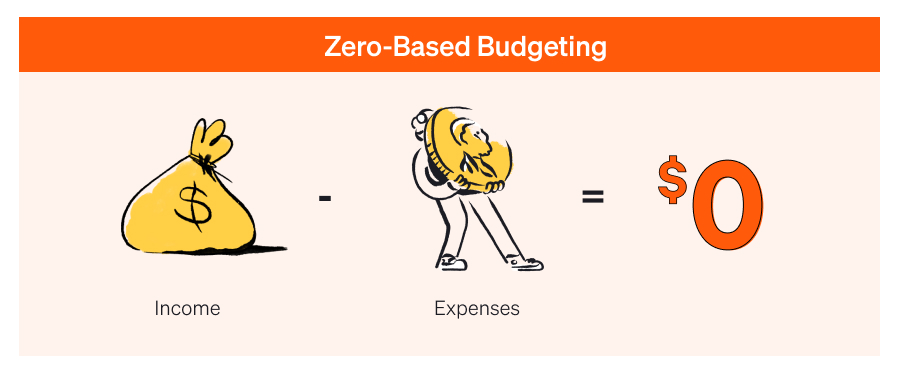

Subsection 2.2.7 The Zero-Based Budget

The zero-based budget is a modern update on the envelope system. Under this system, when you get a paycheck, you meticulously give a purpose to every single dollar. So, you do not have just a “savings” category. You would, for example, say “$50 goes into my rainy-day fund. $50 goes into my retire savings. $20 goes into my fund for a vacation.” Beyond paying for your necessities, there are no requirements on how much goes where.

The benefit of the zero-based budget is for you to meticulously track your spending. No dollar goes unaccounted. Many people find it helpful in recognizing over-spending habits and starting to save more.

The zero-based budget requires a lot of work and dedication. Have you ever tried tracking calories for even just a week? It’s hard and tedious. It’s the same thing here. Every dollar you spend needs to be recorded and tracked. Many people are unable to keep up with the recording, which makes this budget useless. Also, some users of this budget method do not increase their savings amounts and instead simple spend their entire paychecks. Ultimately, it is not really a beginner-friendly approach to budgeting unless you have the disciple to stick to it.